Despite Changes, Grocers Expect Meat Sales to Grow

Make no mistake: Changing eating habits are taking their toll on meat sales, gradually chipping away at animal protein’s longtime dominance at center of plate.

Yet the greater willingness of consumers to try alternative proteins and the advancement of plant-based meat substitutes don’t seem to have quelled the confidence of grocery retailers in the success of their meat departments, at least for the foreseeable future.

That’s according to the results of Progressive Grocer’s latest Retail Meat Review, an exclusive survey of retailers that expect continued meat sales growth, despite pricing challenges and the rise of alternative products.

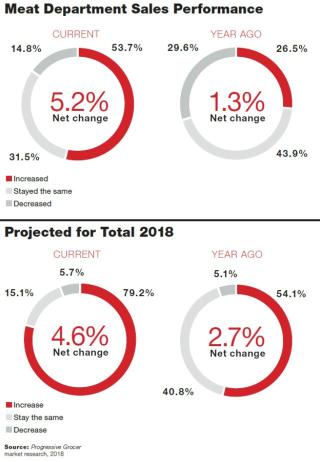

In fact, nearly 80 percent of survey respondents expect their meat sales to increase during 2018 compared with 2017. Just under 6 percent expect sales to decrease, while about 15 percent anticipate that sales will stay the same.

“Meat sales will increase, as I am pushing forward with even more deals, and have added some more smoked meat space in another area,” Tony Orlando, owner of Tony O's Supermarket & Catering, in North Kingsville, Ohio, tells PG.

In the past year, “deflation caused a slight drop in sales, but our tonnage remained about the same,” Orlando notes. “We will stay very aggressive and keep buying in big when the market drops, and post a ton of deals on Facebook and our website.”

To be sure, a full-service meat department with diverse offerings and knowledgeable staff prepared to go the extra mile to delight shoppers are key points of differentiation for independent grocery retailers like Tony O’s.

But that confidence isn’t unanimous, as competition continues to mount in many markets.

“We cycled a competitive closing in July, and started seeing declines as the economic environment got more difficult,” says A.J. Swander, store director of the SpartanNash Co.’s Family Fare supermarket in Manistee, Mich. “The big box [Meijer] also struggles for sales, so the competition heated up, and our sales are flat to slightly declining in meat.”

High Stakes

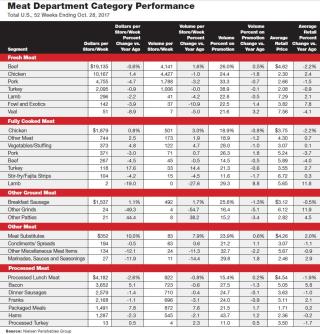

Looking at the broader market, overall U.S. supermarket sales of fresh meat fell 0.6 percent in dollars, to $36.6 billion for the year ending Oct. 28, 2017, while weekly volume per store fell 0.4 percent, according to the Nielsen Perishables Group.

“Across the board, grocery’s meat department still felt the residual effects of 2016’s price deflation,” says Sarah Schmansky, VP of fresh growth and strategy for Chicago-based Nielsen. “In 2017, we saw average prices decline within stores, causing overall dollar decline, coupled with minimal positive movement to increase overall tonnage. That said, beef continues to rebound and slowly capture additional volume – just not enough yet to move the entire department.”

Retailers indicate that pricing will continue to be a struggle, especially as they contend with competitors.

“We expect another decrease, as another tertiary competitor will be opening,” Swander tells PG. “Our market [northern Michigan] is very competitive and will continue to be so, with sales so hard to come by.”

Meanwhile, Scott Karns, CEO of Karns Foods, in Mechanicsburg, Pa., expects his meat sales to “increase, with expected slight cost increases.”

But perhaps more significant than economics is the emerging sea change in the way that folks eat.

“The good news is that protein continues to be a hot topic, and an important attribute for many consumers and their well-being,” Nielsen’s Schmansky says. But while 78 percent of consumers see meat as their primary source of protein, according to Nielsen data, “we’re starting to see a shift occur,” she observes. “Consumers are looking beyond the traditional meat department to fulfill their protein intake.”

In fact, 22 percent of consumers intend to eat less meat over the next year, according to Nielsen’s protein survey, and in turn, move to seafood and plant-based alternatives.

“There is a knowledge gap to be filled here – to reinforce to consumers that meat is a high-protein option,” Schmansky says. “Currently, about half of all shoppers don’t give meat the credit it deserves within their protein rotation.”

Sprouting Sales

While plant-based meat alternatives are one of the hottest topics on everyone’s radar, it’s still a very small percentage of overall meat sales.

That said, Schmansky advises that “it is important to keep a close eye on the amount of consumers turning to overall plant-based foods to improve their well-being, which is taking dollars away from this department.” According to Nielsen data, 39 percent of Americans are actively trying to incorporate more plant-based foods in their diets. This trend is being driven mainly by young, multicultural consumers who desire to improve their overall health and nutrition. And with 15 percent of total food and beverage sales coming from products that meet a plant-based diet, the options are increasing.

“However, with change comes a learning curve and an opportunity for grocers: Consumers have noted that eliminating meat altogether is a challenge, with 36 percent saying it’s hard to prepare a meatless meal,” Schmansky says.

It’s another opportunity for grocery retailers to own another part of the wellness equation – offer preparation guidance for plant-based products, and have meat managers collaborate with in-store dietitians to create meal plans that incorporate plant-based meat alternatives. This will go a long way toward demonstrating a commitment to shopper needs and keep them from shifting their loyalty away from your banner as their eating habits evolve.

Nearly half of the retailers who responded to PG’s survey carry plant-based meat alternatives, with about a quarter considering adding them to their product mix. Just over half say that they do or would merchandise these products alongside animal proteins in the meat case.

Follow-up responses suggest that the availability and positioning of plant-based meat substitutes will reflect local demand for them, particularly among smaller, independent grocers.

Karns Foods doesn’t offer them in its meat department, “but feel[s] it will grow in its own department and set,” Karns says. At Michigan’s Family Fare, meat substitutes are currently confined to the frozen aisle, Swander notes: “They are a small portion of sales, but do OK when promoted.” Meanwhile, Orlando asserts that they’re “not something I do.”

Price, Quality, Service

Despite the changes that may someday transform the traditional meat department into a broader protein destination, in the here and now, selling meat still comes down to three basics: pricing, quality and service.

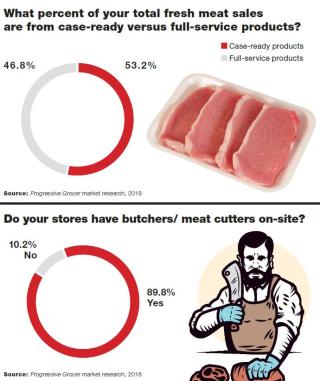

Nearly nine out of 10 PG survey respondents employ in-store butchers, and nearly all stress this to their customers as a point of differentiation. Even so, respondents say that their case-ready offerings edge out the service counter as a percentage of overall meat sales, suggesting that time and convenience are still important to shoppers.

“This market is promotional pricing, quality and everyday pricing,” Family Fare’s Swander affirms.

At Karns Foods, “it’s still all about pricing to drive sales, but [consumers] are accepting value-added price increases if it saves them time,” Karns says. “Customers are looking for more meal-ready items that have some prep work completed, but still allow home cooking. Additionally, customers are looking for new options.”

Tony O’s is “a custom-cut store, and there are not many of us are left,” Orlando boasts. “In my area, price is king, and I have the best prices in the county, which I remind my customers of all the time. We also lay out our case differently each week, and sometimes I will switch up the case different for the weekends, and even more, if I find a crazy deal.”

He adds: “I buy big and sell big in large displays, which brings in more sales with good profits. A well-run independent can outmaneuver the big stores quite easily, as I can change the case as needed, with no central planning from headquarters.”

But although the basics are still ruling the day, meat managers must prepare for a very different world that looms in the near future.

“Sustainability and health attributes will continue to be a driving growth factor in the meat department through 2018,” Schmansky says.

According to Nielsen data, 31 percent of consumers are willing to pay more for ethically raised meat, resulting in claims like ABF (antibiotic-free), hormone-free, natural, vegetarian-fed and grass-fed showing positive dollar and volume growth.

And even with newfound consumer interest in these claims, Schmansky asserts, organic meat varieties will continue to play an important role in overall meat department success.

“We know that retailers winning in the fresh meat space are increasing their assortment of organic fresh-meat options,” she says, “and roughly 9 percent of total meat dollar sales come from organic items in these top-performing retailers.”