Consumer Expenditures Study: Shopper First Is Best Strategy for Success

Discover the 2019 Data

It’s no surprise to anyone that the pace of innovation in grocery retailing has accelerated, and for the good of the industry, let’s hope it stays that way.

The announcement of Amazon’s acquisition of Whole Foods Market may be a fading memory, but it won’t ever be forgotten, and it ought to be the first thing retailers see in their rear-view mirrors when thinking about what they should do next.

A year ago, we noted that understanding how consumers shop has become more important than exactly what they’re buying (though that’s certainly helpful to know, as the data that follows in this report demonstrates). But continuing to grow in importance is the why — the motivation behind increasingly personalized buying and eating habits.

The Food Marketing Institute (FMI) in June released the 45th edition of its annual “U.S. Grocery Shopper Trends,” a look at grocery shopper attitudes and behavior. The 2019 report, a survey of nearly 1,800 grocery shoppers prepared by The Hartman Group Inc., studies what consumers want from their retailers when personalizing their grocery shopping.

To achieve this personalized shopping, consumers visit an average of 4.4 banners per month and regularly shop 3.1 channels to meet their diverse grocery needs. They also expect their grocers to evolve with these needs, and to be satisfied with their primary store’s ability to meet those needs (8.7 out of 10).

As for choosing a store, quality, freshness, low prices, cleanliness and product variety are the keys to retaining shopper loyalty.

IN-DEPTH ANALYSIS

Read our in-depth analysis of some of the better-performing categories in this year's study, including:

Convenience is driving younger consumers to shop online. Shoppers rank their online experience slightly better than those in physical stores when it comes to transparency, convenience and personalization, but online isn’t cannibalizing in-store visits — the 43 percent of consumers who shop online also average 1.7 trips a week to their physical stores, higher than the national average of 1.6 trips per week, making the in-store experience an important component of the omnichannel environment.

These desires for both convenience and discovery, FMI reports, also lead to shoppers experimenting with more personalized methods for retrieving their groceries, such as delivery or click-and-collect methods.

“‘Trends’ explores the current food retail marketplace and the influential roles health, well-being and technology play in the experience,” Sarasin says. “Food shopping is personal, and grocers help their shoppers navigate shifting needs, values, priorities and life pressures that require teamwork, negotiation and compromise at home.”

Moving Past Price

Consumers enjoy the shopping experience more when they believe they’re getting something special or out of the norm, even when they’re not, David Moran writes in "Moving Past Price: A Guide for Modern Promotions."

Moran cites a recent study revealing that 94 percent of Americans indicated that they would take advantage of an exclusive offer if it weren’t typically offered to the general public. Survey participants selected this option over a price-match guarantee, and 41 percent said that they would likely seek out something to buy just to use the offer.

Digital coupons and in-store promotions can work together to create a single, cohesive shopper journey, regardless of whether that journey is motivated by months of product research or an impulse buy. “It’s possible to use digital coupons to inform and stimulate in-store purchases in creative ways, and vice versa,” Moran says. “These insights can then be used to better predict in-store and online engagement.”

Another vital piece of the marketing technology puzzle for retailers and CPGs is artificial intelligence. AI, machine learning and data analytics are being applied to inform marketing and pricing decisions, Moran observes.

“AI analyzes millions of different data points remarkably fast to deliver the information needed to drive promotions,” he says. “Systems parse data in very specific ways, enabling brands to maximize their potential. Promotions become far more customized, which places them in a better position to be redeemed, whether based on a shopper’s momentary whim or by winning on price. Intelligence, coupled with predictive analytics, offers an unparalleled level of flexibility.”

Retailers would be foolish to ignore any technology or technique that helps them better understand shoppers’ behavior and predict how their needs can best be met. Doing so accurately and consistently is the formula for inspiring loyalty and driving sales.

Sales Snapshot

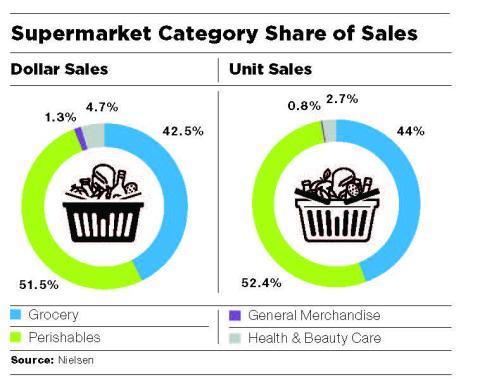

Total supermarket sales across all grocery, perishable, general merchandise, and health and beauty categories topped $420.9 billion, a 2.1 percent increase from 2017, Nielsen data shows. Individual products sold surpassed 146 billion, down 0.7 percent from 2017.

Predictably, perishables performed the best and continue to show the most promise for the foreseeable future: nearly $217 billion in 2018, up almost 3 percent over the prior year.

Driving that growth is the deli, with sales up nearly 10 percent over last year. Floral showed the next strongest sales growth, up 4.6 percent to nearly $2.5 billion. Bakery delivered sales growth of 3.6 percent, to nearly $9.7 billion. Meat and seafood followed, with sales growth of nearly 3 percent, at $53 billion, chased by produce (up 1.4 percent), frozen foods (up 1.3 percent) and dairy (up 0.9 percent).

Key categories in perishables include prepared foods, beverages, eggs, desserts and dairy alternatives.

Grocery sales rose 1.5 percent, just clearing $179 billion. The strongest growth among subcategories was in alcohol, with sales up nearly 3 percent to $24.3 billion.

The $127 billion grocery food category rose 1.5 percent in sales over the prior year, with few significant standouts. Nonfoods remained flat, meanwhile, with sales up 0.4 percent to $27.8 billion.

Health and beauty care is up 1 percent, to $19.8 billion in sales. Strengths include baby products, ear care and vitamins. General merchandise brought up the rear, with sales down 2.7 percent, at $5.4 billion.

View the 2019 data and then read our in-depth analysis of some of the better-performing categories in this year's study, including:

For the 2019 Consumer Expenditures Study, data has been provided via Nielsen’s Total Food View, an inclusive data universe of UPC and non-UPC products (which includes fresh random-weight retailer-assigned PLU [price lookup code] and system 2 sales volume). This reflects the total U.S. food market, which encompasses all grocery stores with $2 million or more in annual all-commodity value (ACV), and includes natural food retailers and discount grocers. References to “fresh” or “perishable” foods encompass the inclusive view of UPC-coded and non-UPC products found throughout the store, but most predominantly in the produce, bakery, deli, meat and seafood departments.